You may not have your own house with a loan (as yet) but that doesn’t mean that you cannot avail of tax benefits. Even if you are staying on rent and your company is paying you house rent allowance (HRA) you can avail tax benefit. Many a times, your company’s HR department does the tax calculation for you, which is a great convenience, but it is always a good habit to know how the expenses can be deducted from your income so as to reduce your tax liability. Of course this benefit (exemptions) can be availed only if you follow the existing tax structure. Let me illustrate how much can be shown towards expenses. The least amount of the following three is considered eligible for the benefit: 1. Actual HRA received (per annum) 2. Actual rent paid (per annum) minus 10% of your salary (per annum) 3. If you are staying in a metro, then 50% of your salary or 40% of your salary Now let us work out an example: > You are staying in Mumbai and your salary is Rs 25,000/- per month > The HRA received from your company is 12,000/- per month > Rent is Rs 10,000/- per month Now, the calculation: 1. HRA received: 12,000 x 12 = 1,44,000/- 2. Rent – 10% salary: (10,000 x 12)-( (25,000 x 12)*10%) = 1,20,000 – 30,000 = 90,000 3. Staying in a metro: (25000 x 12) x 50%= 1,50,000/- So the least of the above three is point # 2. Rs 90,000/-. You are allowed to deduct this amount from your Income u/s 80 GG. This is how you can verify your tax statement. For detailed calculations, do take support of your CA or financial consultant. Thank you, Anand Mhapralkar Certified Financial Planner^CM http://www.AnantWealth.com

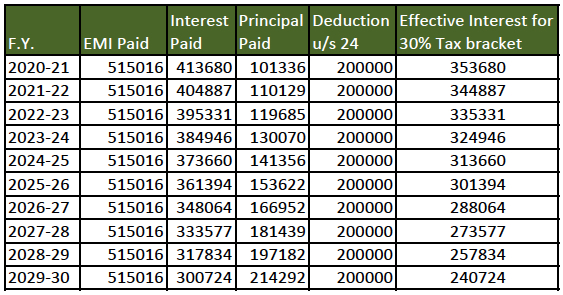

Almost everyone who dreams to own a home in Mumbai has to opt for a housing loan, given that the astronomical real estate rates in the city are more often than not generally way more than your savings! Buying a housing property in Mumbai does not come easy and cheap. Once you finalise on a neighbourhood and an appropriate size of an apartment well suited to you and your family, you have to look at the most important aspect of home buying—the cost. I would say almost 90 per cent prospective buyers have to opt for a housing loan. Additionally, a housing loan also ensures the bank involvement in verifying that the property is clear of any legal issues. There are a few things one should keep in mind before making such an important commitment: 1. Your total EMI (Equated Monthly Installment) should not exceed more than 40 per cent of your monthly income. 2. Compare the interest rate and check if it is floating or fixed. A floating rate is variable and mostly helpful, as the interest rates gradually go down. 3. Check if it is a repo-linked lending rate (RLLR). Many times, banks do not forward the interest-rate benefit to the borrowers. This new RLLR, on the other hand, will benefit borrowers as the bank will have to forward the interest-rate benefit as and when there are any changes. 4. Check if there are any pre-payment charges. No pre-payment charges makes the loan beneficial to you; try to make a lump-sum payment as and when you get any bonuses or extra profit from business, thus lowering on your interest expenses. 5. There is a tax benefit forwarded to home loans: you can deduct up to Rs 2,00,000/- u/s 24 towards interest payments and 1,50,000/- u/s 80c (this being the total amount which can be exempt under this section). Let me illustrate the example in case of a Rs 50 lakh loan to be paid over 10 years. Loan Amount: Rs 50,00,000/- Loan Date: 1 April 2020 Tenure: 20 years Interest rate: 8.35% Your EMI will be: Rs 42,918/- (Approximate)

It is always better to make a informed decision. Thank you Anand Mhapralkar Certified Financial Planner^CM +91 9820663784 http://www.AnantWealth.com

I have been receiving a bunch of questions about what NAV means so let’s tackle that topic today. NAV stands for net asset value, which represents the net value of a fund. It is the total value of a fund’s assets minus the total value of its liabilities divided by the number of units issued. NAV represents the per unit price of the fund on a specific date, which typically is the closing of the previous market day.

Now let’s go into it a little deeply and further get an insight about NAV and mutual funds.

A fund works by collecting money from a large number of investors. It then uses the collected capital to invest in a variety of stocks and other financial securities that fit the investment objective of the fund. Each investor gets a specified number of units in proportion to their invested amount, and they are free to sell (redeem the value of) their fund units at a later date and pocket the profit—or lament the loss. Since regular buying and selling (the investment and redemption) of fund units start after the launch of the fund, a mechanism is required to price the units of the fund. This pricing mechanism is based on NAV and is always considered per unit.

Unlike a stock, whose price changes with every passing second, mutual funds don’t trade in real-time. Instead, mutual funds are priced based on the end-of-the-day methodology based on their assets and liabilities.

The assets of a mutual fund include the total market value of the fund’s investments, cash and cash equivalents, receivables and accrued income. The market value of the fund is computed once per day based on the closing prices of the securities held in the fund’s portfolio. Since a fund may have a certain amount of capital in the form of cash and liquid assets, that portion is accounted for under the ‘cash and cash equivalents’ heading. Receivables include items such as dividend or interest payments applicable on that day, while accrued income refers to money that is earned by a fund but yet to be received. The sum of all these items and any of their qualifying variants constitute the fund’s assets.

The liabilities of a mutual fund typically include money owed to the lending banks, pending payments and a variety of charges and fees owed to various associated entities. Additionally, a fund may have foreign liabilities; these could be the shares issued to non-residents, the income or dividend for which payments are pending to non-residents, and sale proceeds pending repatriation. All such outflows may be classified as long-term and short-term liabilities depending upon the payment horizon. The liabilities of a fund also include accrued expenses, like staff salaries, utilities, operating expenses, management expenses, distribution and marketing expenses, transfer agent fees, custodian and audit fees, and other operational expenses.

To compute the NAV for a particular day, all these various items falling under assets and liabilities are taken at the end of a particular business day.

Now let’s take a look at some the queries that I get asked by clients and friends:

“I am getting this fund’s units at Rs 10 since it is an NFO (New Fund Offer). I am getting it cheap and I want to invest.”

“I want to invest in mutual fund A with a NAV of Rs 105 as mutual fund B has a NAVof Rs 250. Will it be profitable to buy mutual fund A?”

Consider that there are three mutual fund companies—A, B and C.

All the above funds are investing in just one company’s shares, let’s say HDFC Bank (just as an example). The price at NFO for all the funds is Rs 10 per unit and there are no income and expenses (to keep it simple).

Mutual Fund A was launched on 2 Sept 2016.

Mutual Fund B was launched on 7 Sept 2018.

Mutual Fund C was launched on 4 Aug 2021.

Mutual fund C is offering a unit at Rs 10. Would this be cheap? And will it give more returns than the other two? Please take a look at the chart below.

Fund

Date of Launch (NFO) | Price per unit

HDFC Share price on these dates

NAV on 7th Sept 2018

NAV on 4th Aug 2021

A Mutual Fund

2 sept 2016 | 10 Rs

642.55 Rs

16 Rs

22.89 Rs

B Mutual Fund

7 sept 2018 | 10 Rs

1028.47 Rs

NFO – 10 Rs

14.30 Rs

C Mutual Fund

4 Aug 2021 | 10 Rs

1470.90 Rs

Not yet launched

NFO – 10 Rs.

As per the above table, if one had bought units on 7 Sept 2018 from mutual fund B at Rs 10, or from mutual fund A for Rs 16, it would have given the same returns on 4 Aug 2021. And going forward, if one invests in any of the above funds whatever the NAV, the returns will be similar since it is investing in the same security!

So one needs to understand where the fund is investing and how the underlying security (company)/ or the economy is performing to evaluate the future returns from the investments.

I hope the above explanation and example have made things clear, but if you still have any queries please feel free to call me.

Note: Some technical details were gathered from investopedia and public portals.

Thank you, Anand Mhapralkar CERTIFIED FINANCIAL PLANNER CM +91 9820663784

Now that the second COVID-19 wave in the country is slowly abating and the process of unlocking has been underway, I am sure everyone is breathing a cautious sigh of relief. Work, too, is slowly limping back to normal. And speaking of work and business, today I would like to focus on investing in Mutual Funds!

After reading a few financial articles over these last few days, and getting some queries from my clients, it occurred to me that there were some aspects about mutual funds investing needed clarifying.

The first point is about the IDCW (which I explain in detail below). From the time I started Anant Wealth, I have met clients from various backgrounds, all with a diverse set of goals and requirements. One type of clientele falls in the distribution bracket. This refers to the retirees or people who don’t work for money or earn a salary. Many of the clients from this bracket were in the habit of investing in products which would provide them with dividends as their monthly income. Their understanding of the process was that they were getting a certain amount as interest/dividends and their investment was safe.

A few of them were invested in monthly income plans, where particular dividends are issued every month. They were complaining that their investment value had reduced. This belief has been due to a slight misunderstanding in the terminology that only just came to light, as I explain below.

If you check your recent statement, your schemes/funds that were under the dividend distribution plan are now mentioned as IDCW. This means income distribution and capital withdrawal. This change in terminology was implemented from 1 April 2021 by SEBI ( Do check the AMFI site for more explanation: https://www.amfiindia.com/investor-corner/knowledge-center/FAQs.html ). It was initiated so that the investor understands that it is not the dividend or the interest which is distributed to the investor; it is, in fact, the income received by the fund and in the event of the income being less, then it was a part of capital that was distributed to you. This distribution led to the NAV going down. Therefore, in some cases where the dividend was distributed, the NAV of a scheme had actually decreased. This is because of the amount that is distributed to the investor plus the actual ‘mark to market’ which has reduced the NAV of the particular fund.

It is therefore by keeping such things in mind that I work on an asset allocation strategy, which would work as a regular income- providing corpus as well as give certain capital growth over a period of time. I am happy to say that this strategy, called the Life Line Plan, has worked as intended without giving an illusion to the investor of distributing dividends/interest to the clients. Moreover, the asset allocation works in a way to grow your capital too.

I hope this answers any doubts that you may have had and restored your faith in the importance of investing!

Thank you, Anand Mhapralkar CERTIFIED FINANCIAL PLANNER CM +91 9820663784

In the world of investments, we are used to hearing words such as return on investment, guaranteed returns, very safe to invest, high returns etc. If you are a fearless risk-taker when it comes to investments, then your focus is usually on ‘returns’; on the other hand, if you tend to be more conservative, then it is ‘safety of the capital’ that is your primary aim. Sometimes however, even the fearless risk-taker becomes conservative after burning their fingers. This normally happens if the investments are focused on products, i.e. high returns, and not on the goal and time horizon.

The reason for the above summary of different kinds of investment goals is to lay the groundwork for the topic of this blogpost—inflation and safe investments!

A lot of conservative investors looking to secure their investments while having a long-time horizon should also consider the impact of inflation and how much their hard-earned money will be worth when they actually need it. I have always explained to my clients that all investments come with a risk, even the safest ones;this includes insurance policies that some clients consider as an investment product (as sold by many agents). That may lead you to wonder how a fixed deposit (FD) in a nationalised bank and an insurance product could be risky.

But the reality is that an FD and other safe products, too, come with a risk, which is called the ‘purchasing power’ risk. That means your money, after adding the interest at maturity, will not be as advantageous as it is todayand the insurance product will give you meagre returns. I have seen some of my clients getting 3% to 4% over 20 years, while some policies had a negative return, that too with a long-time term premium paying commitment.That is why it is important to check the real rate of return when investing for the longer term.

The real rate of return = (1 + Return on Investment/1 + Inflation rate) – 1

For example, if the return on investment is 7% and inflation is 5%, then the real rate of return = [(1.07/(1.05)-1]x100 = 1.90% .

Now let us see what happens if the scenario is reversed—if the return on investment is 5% and the inflation is 7%.

The real rate of return = [(1.05/(1.07)-1)]x100 = (-)1.86% . That is a negative return.

Negative returns on safe investments can actually eat up into your capital.

It is therefore important to understand the real rate, to invest wisely, as the inflation rate for different products and services is different and will affect your investment over a period of time. The data that is shared by the official body that looks into these aspects, the Indian Economic Services,may not be usefulfor your calculation. (Take a look at how the inflation rate is derived here: http://www.arthapedia.in/index.php?title=Headline_inflation).

For your calculation, you need to check your expenses over a period of time and check how your expenses are increasing (this will be your inflation rate)and draw your conclusions about the Real Rate of Return on your investments.

The most important aspect about investing, though, is having a clear plan to reach your goals. One needs to have the right asset allocation, taking into consideration the risk profile and time frame of the goals and needs. The investment product should be one of the final steps in the whole process. It is the best way to mitigate risks.

As investment guru Warren Buffett rightly said: Risk comes from not knowing what you are doing!

Thank you, Anand Mhapralkar CERTIFIED FINANCIAL PLANNER CM +91 9820663784

I am writing this blog after almost five months; the last one was my experience of the financial markets over the last decades and how it was impacted in the course of the COVID-19 pandemic at a time of such uncertainty. This much-delayed blogpost is a continuation of that journey. (You can read my previous blogpost on the topic here: https://bit.ly/3ayafam ).

As I had mentioned about my investments during this period, I am still holding on to some part that I had invested to make some short-term profits and to prove a point that market crash is an opportunity if you have a right asset allocation, which I did!

I have to say that one can only learn from his own experience; the feeling of learning from one’s mistakes and discovering the right course of action is very different from trying to gauge the right thing to do based on listening to others—or not doing anything at all!

Speaking of the moves I made, my last tranche—which is still invested—is showing around 87 per cent XIRR (a method used to calculate returns on investments where there are multiple transactions happening at different times). The conclusion one can derive from my experience is to stick to your plan!

Once you plan your investments, either on your own or with the help of a financial planner, you need to be patient and stay the course. I recommend having a certified financial planner to guide you as your behaviour plays a big role in sticking to the plan and having the ideal asset allocation for you.

As a financial planner, I frequently get asked what the right time would be to exit investment portfolios. The answer is simple—there is no right time, unless you need the money to achieve any set goals. If one exits too early, there is a strong feeling of having missed out on a potential golden opportunity, considering a correction in the market; many people, in fact, had to exit from their investments at the wrong time, during the pandemic as they had to meet important financial obligations, unfortunately making a loss.

So link all your financial assets to your goals. Asset allocation is of prime importance. Once you have your goals in place, you know the time horizon for each one and can accordingly ensure you have the right asset allocation to suit your needs.

Speaking for myself, I have not touched any of my investments and I am sure that I will be able to fulfil all my financial responsibilities towards my family—and, of course, still have enough to enjoy every bit of life!

My suggestion based on my experience, therefore, is to have a Financial Plan in place to ensure you take the right decision at the right time.

Thank you, Anand Mhapralkar CERTIFIED FINANCIAL PLANNER CM +91 9820663784

On the face of it, there is nothing about this year that could possibly inspire a feeling of positivity—the pandemic and all the turmoil it has caused, physically, emotionally, and financially. But I have a slightly different perspective on this. And I would like to share my experience about investments and the stock market over these past five months, straight from my heart. These last few months have been a memorable lesson in how the right attitude can help you find opportunity even in the darkest of days. Having pondered over it for a while now and given what the world is going through, I thought it would be a relevant topic to write about. What I have to say is based not just my own experience of making investments, which spans almost two decades, but also on the uncertainty that has gripped all of us over the last few months. And how my learnings as a CFP contributed to my investment decisions. At the outset I would like to state that since I come from a business family, my mind set and approach to investments differs from that of an employed professional. In my working life, I have witnessed three share market crashes, the earliest one being the infamous Harshad Mehta scam. I had very little knowledge about what happened, most of which was from news reports. But what I heard was enough to make me wary of the stock market. Normally, people refrain from getting into it if they burn their fingers once, but after understanding it at a deeper level and the extensive learning from the CFP curriculum, I realized that the stock market can be a reliable source of making money. However, you must have a plan backed by insightful understanding and patience.

When the global COVID-19 crisis started, I was a bit reassured and confident that with my experience and knowledge as a CFP, I would be able to earn some money from the stock market via mutual funds. This was also the time when many people realized the importance of asset allocation. I liquidated some of our debt instruments and Gold investments, divided the amount into four parts, and waited.

I invested my first tranche with NIFTY at 9197 and the second when it was at 8469. After that, NIFTY hit a low of 7500; at that point, everyone thought that it would decrease further. And so we waited some more. Then, the markets started rising and hit 9800. The technical indicators recommended an exit, so I exited one part after making a profit of around 16% (Absolute returns). Now, the profits to the part left invested show returns of around 35% (Absolute returns)! I’m, at the moment, waiting to make my next move. Of course these investments were done considering long-term horizon and according to my risk profile, I am ready to hold this amount for many years without compromising on my other goals. Based on this experience, I have realized that knowledge and experience give you the strength to take discerning, carefully considered decisions and it is up to you to act and reap the rewards. Another thing that I would like to point out is my state of mind at the time. I wasn’t making any hasty decisions out of anxiety. I was disciplined about the plan and executed it patiently. I think that is one of the main reasons that I made a profit. I held on to the funds and waited till they exceeded the returns. I would go so far as to say that this current economic environment helped me learn in a way that no course manual could. It helped me gauge my own nature when dealing with uncertainty. None of this was an easy ride emotionally, as I was second-guessing every decision: Should I invest more? Should I have invested more at the low? Why did I withdraw some at that level? Should I withdraw all to book the profit? Many such questions plagued me with every decision I took. The upside was that knowledge and prior experience allowed me to control my emotions and behaviour. Over the course of these difficult months, I realized the importance of approaching investment with a level head, studying reliable sources for information and then taking a call. There are a lot of people who enjoy giving advice, like agents and brokers. They are always around to tell you all about the rising prices of stocks but instead of believing them blindly and investing in stocks on their say-so, think carefully before making a move. If agents were always right, wouldn’t they have made a lot of money at every turn?

I would like to end my experience by sharing a small diagram that illustrates the various reasons that affect our investments in their order of importance. At the base of the pyramid is investor behaviour, indicating that it has the most impact, while the taxes you pay on the money you earn have the least impact.

Given the significance that behaviour has on investment decisions, always move wisely. Be sure you make a plan, be disciplined in implementing it and be patient as you wait to earn the rewards from it.

Do this and success will be yours!

Thank you

Anand Mhapralkar CERTIFIED FINANCIAL PLANNER CM +91 9820663784

Namaskar, As yet another phase of the lockdown rolls to an end, I hope you and your family are staying safe and staying indoors! We are here now, officially at the end of what would have been the summer holidays, wondering about what could be awaiting us in June. And now even with things slowly easing up little by little, with the government opens some sectors for businesses, we cannot assume that things will resume normally. Relaxing the lockdown, even if it is for certain sectors only, will certainly bring some challenges at our doorstep.

For the past two months now, every one of us has been trying to adapt to this new normal—staying confined to our houses, avoiding socialising, avoiding outdoor activities and basically giving up what we used to take for granted. Many self-employed people, business owners and others have had their avenue of earnings limited, causing them to dip into their emergency/contingency funds (if planned) or using their savings—something that may well go on for some time as things will take a while to normalise.

Being a business owner and a financial planner, I have had the chance to compile a checklist about daily (financial) planning that should hopefully help!

1. Reduce your lifestyle expenses.

2. Since many of you may be using your emergency funds or savings, you need to allocate a substantial amount to replenish these funds. If you do not have a specific emergency fund, please create one. And you can call me anytime if you need to figure things out and plan!

3. Check your medical insurance policies, and be sure you have an adequate one! If not, buy an extra policy to take care of all medical uncertainties. I will explain some points to look at while buying medical health insurance.

4. Same goes with life insurance. Carefully check if you are covered adequately to take care of your family’s future goals.

5. Do remember that once your business resumes, it might not be the same! Temper your expectations. Take baby steps. Think about it as an unavoidable reboot and move slowly with your plans. And remember, every day will bring some new learning.

As mentioned above, here’s a quick list of things to keep in mind when it comes to medical insurance:

Adequate cover: The sum insured should be appropriate to your expected hospital costs. Understand the amount charged at various hospitals.

Check for sublimits / capping on services: many policies have a ‘capping’ on certain services. For example, a capping of 2% per day on the per day hospital room rent. This means that if the sum insured is Rs 5 lakh, you will not be able to spend more than Rs 10,000 per day on your room. So try and avoid a cap if possible.

Coverage of any day care hospital procedures.

Co-payment clause: This means that you have to pay a certain percentage of the total bill.

Pre-existing diseases should be covered. Check according to your requirement.

And most importantly, check your family background for any hereditary illness and get them specifically covered.

The well-being of our families depends on planning all aspects of our life—physical, mental and emotional health, as well as wealth. So if you have not yet planned your finances, please do get in touch with a certified financial planner to understand the importance of financial planning.

And remember—it is always darkest before the dawn! And this challenging time in our lives will also pass soon! Now with the threat of Cyclone Nisarga looming over Maharashtra and Gujarat, it is more important than ever to listen to instructions, stay indoors and remain safe!

Stay strong, stay healthy and plan well, for a steady, prosperous and stress-free future!

Warm Regards

Anand Mhapralkar Certified Financial Planner CM +91 9820663784

It has been over a month since India has not only shut its doors to the world and locked itself down but a lot of things have changed since the COVID-19 health crises gripped the entire world early this year. And after this lockdown as well, a lot more will keep changing. We have always known that life is uncertain! but now it has been proved beyond doubt that things are indeed reallyuncertain!

This pandemic is possibly one of the rare occasions where big as well as small businesses have been affected. And while small businesses with debt might find it tougher to recover, even in this cloud of uncertainty, there is a glimmer of hope. Everyone has come together and is working hard at finding solutions. Even the RBI has come forward to increase liquidity by reducing the repo rate. Of course, only time will tell what will unfold but the upside is that everyone is thinking of ways to keep the economy from sinking. And most people too, though stuck at home, are not sitting idle. Some continue to work as hard, if not harder than, before! Speaking for myself, I have attended so many webinars that I’ve begun wondering if I have become busier than normal!

Staying at home has also brought families closer together (inspite of the fights and arguments!). I have started using digital video platforms to be in touch with family and friends, as have many other people. I believe that such circumstances also provide an opportunity to reassess priorities.

Many business and individuals have started contributing to society. And hopefully, finding our humanity amid the pandemic will make a long-term impact even in the way we go about making profits. It may make people stop indulging in cut-throat competition, or creating a monopoly of products, and may even stop businesses from holding back payments unnecessarily! Good, ethical business practices post the pandemic will be a change for the better!

Being a jeweller and a financial planner, I cannot help but touch upon this uncertainty of markets too.

Equity markets have corrected due to fear and uncertainty but Gold is steadily rising. This is because this particular asset class has always had some negative correlation with equity markets. Given my background, I get to closely analyse both these worlds and having observed it, let me end by striking a cautionary note: Many of us may think that it is a great time to invest—but move slowly and choose wisely. Check both the risk and time horizon for the money you plan to invest. I would say that instead of focusing on returns, now is the time to first secure your family, your home and well-being.

That we will come out of this crisis is guaranteed. It is only a question of when. Until then, we need to find ways to stay safe, secure our families and continue to reassess how we can change for the better when things return to normal.

Namaskar, As I write this, confined to my desk at home, practising staying-at-home, I hope all of you (hopefully reading this from the safety of your homes) are safe and in good health. We are currently passing through extremely difficult and scary times. We have been forced to isolate ourselves from each other, even our friends and neighbours, and stay indoors at a time when the idea of stepping outdoors comes with a huge unpredictable risk. As stressful and depressing as it is to get used to, we need to cooperate with our respective governments and civic authorities, and do what we can to reduce their burden. Because all these stringent policies are meant to keep us safe and healthy. Putting our lifestyle on hold will be challenging, but it is important that we acclimate ourselves to the circumstances now so that we can all hope to see a healthier, safer world tomorrow. Now is the time to spend this time with family, slow down your hectic pace, relax and do some inner reflection. Even if physical activity may be restricted, you can always keep your mind active! I would like to share with you some of the things that I have put on my to-do list as I sit at home.

Play board games with the family, which I wasn’t able to find time for before. My pick is Scotland Yard and Monopoly.

Try my hand at cooking.

Clean the drawers and cupboard, things over which I always procrastinated.

Read more books.

Watch the movies and series I have missed! (But avoid too much of it)

Take a look at important and financial documents and rearranging them if required. (Make a list for easy reference.)

Discuss family goals and plan new ones, be it personal or financial.

Keep in touch with loved ones via a video chat app. (Some apps even allow group video chats.) You too can follow some of these suggestions, or strike off what has been pending on your to-do checklist. But the important thing is to not waste this time and not give in to boredom and laze the days away! I hope and pray that we all come out of this pandemic stronger and a little bit wiser. But for now, stay home, stay safe and stay mentally active. God bless us all. May our doctors, nurses and governments find the strength to fight this! Thank you Anand Mhapralkar Certified Financial Planner +91 9820663784 http://www.AnantWealth.com

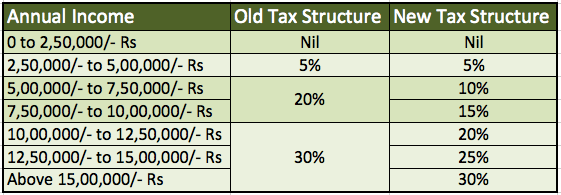

Some might think this is a delayed article but I think it’s right on time! Every year around February, all taxpayers wait with bated breath for the annual budget announcements and look forward to the benefits they can avail of in the coming year. The day the budget is presented, it leads to a lot of confusion about what exactly has been announced. It is only in the following days when more clarity is given that things get settled. Once that is done, you are prepared to start planning your taxes by April, the start of the new financial year. So before April comes upon us, I thought it would be a good idea to quickly run through my analysis and the way forward for the 2020-2021 financial year. This year’s budget axed a lot of hopes of tax rates being lowered or the tax-paying process being simplified. At first glance, the government has indeed introduced reduced tax rates—but with a big condition! You can enjoy this reduced rate only if you forego most of the exemptions and deductions that you avail of. Let me list the deductions which you will have to do away with if you opt for the new tax structure. 1. Standard deduction: Rs 50,000/- 2. House rent allowance (HRA): Amount depends on salary / rent / HRA received / location 3. Housing loan interest: up to Rs 2,00,000/- 4. Investments U/S 80C 5. Leave travel allowance 6. NPS contribution 7. Medical insurance premium: Rs 25,000/- and Rs 50,000/- for senior citizens 8. Savings account interest U/S 80TTA: Rs 10,000/-, Rs 50,000/- 80TTB for senior citizens 9. Interest on education loan and there are several more. Also listed below are some of the exemptions which are allowed: 1. Agricultural income 2. Income from life insurance 3. Retrenchment compensation: up to Rs 5 lakh 4. Voluntary retirement scheme: up to Rs 5 lakh 5. Leave encashment on retirement: up to Rs 3 lakh

Given here are the new tax slabs and rates:

I had hoped that this budget session would see the announcement of more benefits to people investing for the long term, as around 34% of our population is the youth (between 15 and 34 years) and totalling around 90% under retirement age. (Source :Office of the Registrar General & Census Commissioner, India). The previous generations were taught to save but the newer generations need to be taught to invest for their future, as our country does not have any system of offering social security. It therefore becomes important that they learn to take care of themselves when they stop earning. Even now, the government is reducing its contribution towards pension and other such schemes for employees holding government jobs. So, in conclusion, the best option, according to me, is for the earning and the young population to stick to the old tax regime, invest wisely for their future goals and avail exemptions. But the retired / senior citizens should check if they are able to save on tax by shifting to the new tax regime. At the moment, we may be facing some grave political upheavals, as well as this serious global health crisis with the coronavirus epidemic, so it may seem unnecessary to think about personal financial goals given the big picture. But there is never a good or a bad time to think about taking care of yourself and about your future. It is when you are secure that you can think of doing something that can help others. So do not put off sitting down with your financial consultant. And I’m always just a phone call or message away to help you understand what’s beneficial for you! Stay safe, be secure and plan smart! Anand Mhapralkar Certified Financial Planner^CM

Gold, the yellow metal, desired by everyone and considered as a universal currency. Gold prices tend to rise over a period of time and is a good instrument which hedges against inflation but these few years it has shown a drastic increment. Now in 2020 it is at 41500 which was 31450 in 2018 so it has shown around 15% growth (CAGR) in two years. But if taken a longer horizon for like 10 years the returns are around 8% CAGR.

Recent rise in pricing was somewhat linked to the trade war between The East and The West and now ongoing virus outbreak in China which is posing a risk on the world trade. This Tuesday 18/02/2020 United States imposed tough economic sanctions against a Russian oil giant that is keeping Venezuela’s ruling government afloat, which added more fuel to the prices going up.

One should always consider Gold as some component of their investment portfolio and systematically keep buying in small quantities.

(My quote about rising Gold prices published in today’s (20 Feb 2020) Maharashrta Times page 12. Do take a look)